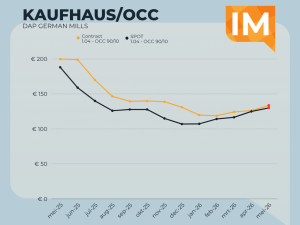

OCC sees a slight increase in price in the first part of the month. We expect further upward development in the weeks thereafter. Available volumes will be scarce. For buyers: secure you tonnage.

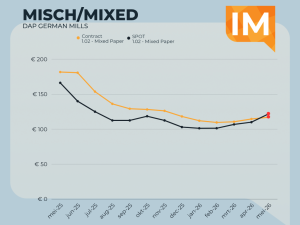

Mixed paper index-based prices will marginally improve in May. In our opinion, the spot rates will overtake the contract prices by 10 euro per ton, which will cause scarcity in mixed paper quickly.

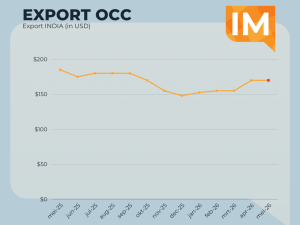

Export prices to India remain stable for now. Joint effort from Indian buyers helps to flatten the price development for now.

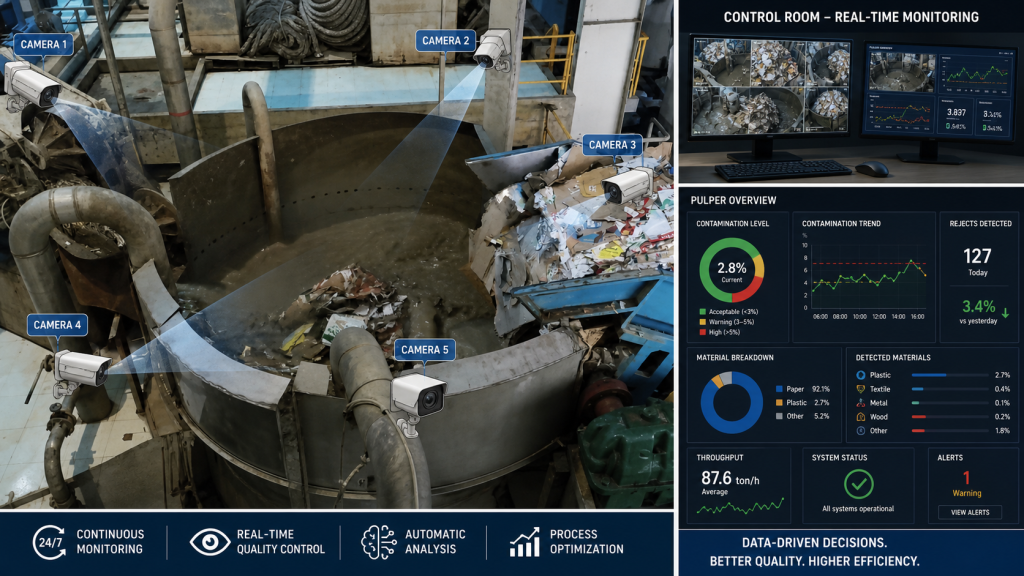

Artificial intelligence is rapidly making its way into the recovered paper industry, particularly in quality control. Where sampling and human assessment still dominate today, self-learning camera systems now enable continuous and objective analysis of material streams. This is no luxury: recovered paper streams are becoming more complex, contamination more subtle, and quality requirements increasingly stringent. AI can measure, recognize, and compare 24/7—delivering a level of consistency that manual processes simply cannot achieve.

The real impact lies in the shift from retrospective inspection to immediate adjustment. Deviations become visible in real time, allowing processes to be corrected more quickly and ensuring more consistent quality. At the same time, disputes over rejections decrease, simply because quality becomes measurable and substantiated by data.

The investment is significant. A fully integrated AI system at industrial scale requires an estimated €2 to €3 million. This includes not only cameras and software, but also process integration, data processing, and structural optimization. It is therefore a strategic decision, not a standalone upgrade.

For recovered paper suppliers, the impact may be even greater than for processors. Quality becomes fully transparent and objectively recorded. This leaves less room for interpretation or negotiation and creates a direct link between measured quality and price. Suppliers who consistently deliver clean and homogeneous material will benefit. Those who do not will see the consequences more quickly and more sharply in rejections and pricing pressure.

As a result, the trade is shifting from relationship-driven to data-driven. Historical performance becomes visible, benchmarking becomes easier, and contracts will increasingly adapt to measurable quality parameters. Discussions may decrease, but the bar will be structurally raised.

AI in quality control is therefore not merely a technical optimization, but a fundamental transformation of the value chain. What was once a gray area is becoming black and white—and that is where the real impact lies.

The recovered paper market is more global than ever, yet negotiation remains surprisingly local. This is driven not only by culture, but also by how markets are structured in different regions. Those operating internationally are not just negotiating price and volume—but also navigating entirely different sets of rules.

In Europe, the market is fragmented and competitive. A large number of suppliers, traders, and highly fluctuating volumes result in a direct, sometimes tough negotiation style. Europeans tend to be straightforward, push boundaries, and occasionally let emotions play a role. At the same time, there is a certain “on/off” mentality: outside working hours, communication often stops.

India presents a completely different picture. The market is highly fragmented, with many small, often family-run mills and a significant role for intermediaries (“indenters”). In this environment, negotiation is less about a single conversation and more about network and timing. Parties move with market sentiment—and when the market declines, they may just as easily disappear temporarily. At the same time, there is considerable alignment among participants, allowing price levels to spread quickly.

The United States represents a more closed system. The domestic market is strong, with exports concentrated through a limited number of ports. American parties negotiate with confidence: direct, results-driven, and willing to take risks. Think of shipping without fixed orders, based on the expectation that the market will absorb the volume. This can make them difficult to read, but also quick in decision-making.

China is the opposite of fragmentation. The market is highly industrialized, with large players operating exclusively at scale. Negotiations are efficient and clear: intentions and capabilities are explicitly stated. However, the threshold is high—small volumes are irrelevant. Real negotiation only begins at substantial tonnages, and those who cannot meet them simply do not get a seat at the table.

Pakistan sits somewhere in between but is developing rapidly. The market is dominated by several large groups and faces significant logistical challenges between port and end user. In negotiations, the price-driven approach stands out: the first question is often the lowest price. Counteroffers are limited, but agreements are generally honored. Availability and rhythm differ—Friday is largely inactive, while the rest of the week is not.

These differences have a direct impact on trade. Where there is still room for nuance and relationships in Europe, China focuses on scale and clarity. India revolves around network and timing, the US around speed and boldness, and Pakistan around price discipline and execution.

Successfully negotiating internationally in recovered paper therefore requires more than just market knowledge. It demands the ability to switch between styles—and to understand that the same deal, in a different region, is concluded under entirely different rules.

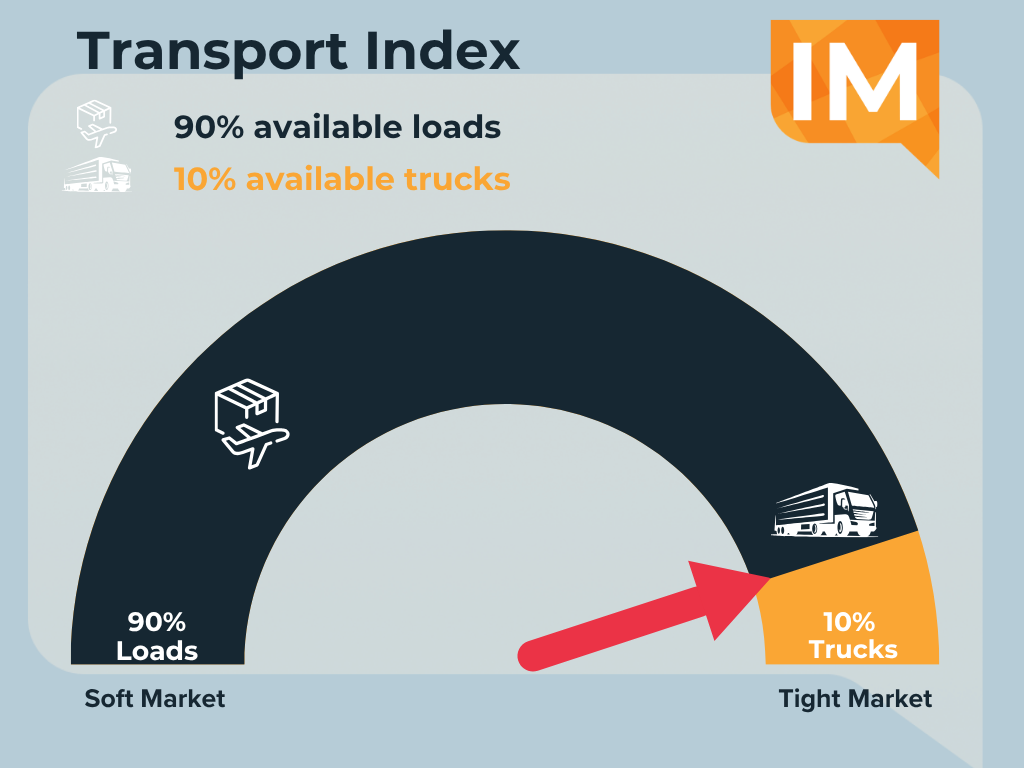

Every year, logistics slows down in April and May. This is not an incident, but a recurring pattern. Public holidays, vacation periods, and a peak in industrial activity reduce available capacity just as demand for transport increases. Drivers are scarce, schedules slip, and ports become congested. The result is a classic transport bottleneck—predictable, yet difficult to manage.

Low-value goods such as recovered paper are hit hardest. This is no coincidence. Recovered paper is a typical “filler commodity”: easy to load, stable in weight, and without time-critical destinations. At the same time, the value per ton is relatively low and transport rates are limited. In times of scarcity, capacity naturally shifts to goods with higher margins or urgency. In addition, recovered paper is more frequently rejected or rerouted, creating additional uncertainty and inefficiency in planning—something carriers have little room for during peak periods.

Companies try to mitigate the impact in various ways. Inventory levels are temporarily increased, transport is booked earlier, and alternative routes or modalities are used more often. Relationships with regular carriers also become more important: those who consistently provide volume are more likely to receive priority when capacity tightens. At the same time, it remains a balancing act between cost and certainty.

The question also arises whether the situation is being exploited. To some extent, yes. Scarcity drives up prices, and carriers logically prioritize the most profitable shipments. But within the trade itself, timing is also used strategically: delays are sometimes leveraged or used as grounds to renegotiate terms. When the market tightens, the balance shifts.

For companies, the key challenge lies in preparation and flexibility. Securing capacity early helps, but offers no guarantees. Spreading volumes, working with multiple logistics partners, and building buffer capacity can reduce risks. Equally important is transparency in the supply chain: knowing where materials are and how vulnerable a schedule is allows for quicker adjustments.

The spring transport bottleneck is therefore no longer a surprise, but a structural feature of the market. For recovered paper—as a typical filler stream—this means logistics will come under pressure every year. Not because the product is difficult, but precisely because it is so easy to move—and therefore the first to be displaced when capacity becomes scarce.