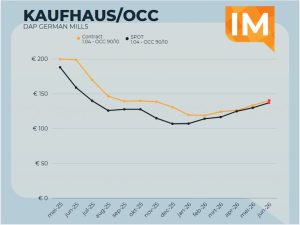

OCC / Cardboard

Last month, OCC was delivered to German mills at prices ranging from €125-150 per mt. It should be noted that the higher ranges were largely spot market prices, mainly paid by mills in Eastern Germany. By purchasing material outside their traditional collection areas on an ex-works basis, these mills appear to be trying to prevent further price increases from developing in the market.

Despite this, there does not seem to be an excessive amount of OCC available. The tight transport market has not helped either and may have created a somewhat distorted picture of actual supply. This week will be crucial in determining whether sufficient volumes are available to satisfy demand from all consumers.

For June, prices appear stable to slightly firmer. We expect OCC prices to settle in the range of €130-140 per tonne delivered mill. In addition, we believe there is still room for some “extra” premiums to emerge in specific regions or for immediate deliveries.

EUWID contract prices for May were reported at €132-137 per tonne and are expected to increase by another €6-9 per tonne during June. This would result in contract prices moving into the €139-145 per tonne range, which will inevitably have an impact on spot market pricing as well.

Mixed Paper

Mixed paper has become noticeably more sought after over the past few months. Stronger demand from the deinking sector has translated into increased demand for mixed paper grades across the market.

Market prices for mixed paper during May ranged between €115-128 per tonne, while EUWID contract prices lagged behind at only €110-117 per tonne. As a result, we expect a significant correction in the June contract settlements, potentially adding at least €10 per tonne.

Mixed paper continues to be a challenging grade to define and categorize. Collection systems vary considerably between regions and countries, resulting in substantial differences in quality and composition. This makes direct price comparisons increasingly difficult.

For June, we expect market prices to move into a range of €122-135 per tonne, while EUWID contract prices are likely to remain slightly below spot market levels at approximately €122-129 per tonne.

Export OCC

India was notably absent from the market during most of May. The first two weeks saw reasonable purchasing activity, but during the remainder of the month buyers were largely nowhere to be found.

At the beginning of May, OCC 95/5 was trading around USD 170 per tonne. Subsequently, several mills attempted to push prices below the USD 165 per tonne level, but these efforts were unsuccessful.

Since then, the market has recovered. Prices for OCC 95/5 have moved back above USD 170 per tonne, and trading activity has slowly resumed. While volumes remain modest, buyers have started returning to the market.

We expect additional upward movement during June. The purchasing gap created by the absence of Indian buyers in the second half of May will eventually need to be filled, and mills may find themselves returning to the market at a time when available volumes are less abundant than anticipated.

Indonesia has significantly increased inspections of imported waste streams in recent weeks. Plastic waste and mixed paper shipments are receiving particular attention, with containers being opened more frequently and, in many cases, held at ports pending further inspection.

For the recovered paper market, the stricter scrutiny of mixed paper grades is especially noteworthy. According to market sources, authorities are focusing primarily on shipments originating from Europe and North America. Many single-stream collected mixed paper grades still contain considerable levels of contamination, ranging from plastics and packaging materials to other non-paper components.

The background to these developments can be traced back to the global shift in waste flows following China’s import ban in 2019. Since then, larger volumes of recyclable materials have been redirected to Southeast Asia, including Indonesia. Local governments and environmental groups have increasingly raised concerns about the environmental impact of contaminated imports, particularly their contribution to pollution and waste management challenges.

Reports from the market suggest that a substantial number of containers are currently being held at Indonesian ports, while significant volumes are still on the water and destined for the country. This has created uncertainty among exporters, importers and shipping companies alike. As a result, traders are actively exploring alternative destinations and discharge ports for shipments that may encounter difficulties upon arrival.

While the measures affect various waste streams, paper exporters are also experiencing longer inspection times and increased uncertainty surrounding ongoing shipments. For some market participants, this may lead to delays, additional costs and temporary disruptions to established supply chains.

For the recovered paper industry, the situation serves as another reminder that quality requirements continue to evolve. Importing countries are paying closer attention to the actual contents of containers, and materials that may have been accepted in the past are now subject to far stricter scrutiny.

We will continue to monitor developments closely. Whether this proves to be a temporary enforcement campaign or the beginning of a structural policy shift remains to be seen, but one thing is already clear: Indonesia is currently taking a much tougher approach to waste imports.

This year marks an important milestone for the Dutch recovered paper industry. FNOI, the Dutch association representing recovered paper collectors and traders, celebrates its 75th anniversary.

At a time when many trade associations are merging into larger organizations or broadening their focus, FNOI remains one of the few industry associations dedicated entirely to the recovered paper sector. Its continued relevance is reflected in its membership, with approximately 70 companies still actively involved.

Over the past 75 years, both the industry and the organization itself have changed considerably. International markets have expanded, supply chains have become increasingly global, and the role of industry associations has evolved. FNOI has successfully transformed itself from a traditional trade association into a vibrant networking platform where industry professionals meet, exchange ideas and strengthen business relationships.

The anniversary also marks a change in leadership. Gerard Nijssen has stepped down as chairman, handing over the role to Marc van Gerrevink. Several new board members have also joined the organization, ensuring a fresh perspective as the association moves into its next chapter.

The 75th anniversary was celebrated during a well-attended event in Hoofddorp. Early in the evening, attention was given to the history of the organization, its achievements and the transition within the board. As the evening progressed, however, the atmosphere became increasingly festive.

Anyone present quickly discovered that the recovered paper industry is not only capable of working hard but also of celebrating properly. Collectors, traders and industry partners filled the dance floor well into the evening, proving once again that strong business relationships are often built both inside and outside the workplace.

We would like to congratulate FNOI on reaching this impressive milestone and wish the organization continued success for the years ahead!

The bankruptcy of Coldenhove Paper Mill in Eerbeek has sent shockwaves through the Dutch paper industry. Not only because more than one hundred jobs are at stake, but also because another company with a long and proud history has disappeared from the sector. Coldenhove had been producing paper since 1661. Companies like that do not simply disappear; they are part of the industrial heritage of an entire region.

Unfortunately, the bankruptcy fits into a broader trend that has been unfolding across Europe for years. Manufacturing paper in Europe has become increasingly challenging. Energy costs, labour expenses, environmental regulations, financing costs and maintenance requirements are all significantly higher than in many competing regions. At the same time, Asian producers—particularly in China—often operate on a scale that European mills simply cannot match.

The contrast is striking. While many European paper machines produce between 100,000 and 300,000 tonnes per year, some of China’s newest paper machines exceed one million tonnes of annual production capacity. Such scale creates substantial cost advantages. Larger production runs, lower fixed costs per tonne and highly integrated supply chains allow these mills to compete aggressively in global markets.

Historically, European producers have compensated for this disadvantage through quality, innovation and specialization. Coldenhove itself was a good example of this approach. The company focused on specialty papers, serving niche markets where technical expertise and product performance mattered more than volume. For many years, that strategy proved successful.

However, the market continues to evolve. Even specialty paper producers are facing growing pressure from rising costs and increasing international competition. The uncomfortable question is whether specialty paper manufacturing in Europe still has a long-term future.

The answer is probably yes—but not for everyone. Mills with sufficient scale, strong customer relationships, specialized products and efficient operations can still thrive. Companies that are caught somewhere in the middle, neither large enough to compete on cost nor specialized enough to command premium prices, face a far more difficult future.

The Dutch paper industry offers a clear illustration of this reality. The list of remaining paper producers continues to shrink. Papierfabriek Doetinchem remains one of the few mills still producing paper in the Netherlands. Companies such as Solidus, ESKA and FBB are primarily focused on board production, while Smurfit Westrock Parenco in Renkum continues to manufacture recycled paper grades, including newsprint and fluting. Compared with previous decades, however, the sector has become considerably smaller.

For several German manufacturers, Coldenhove’s disappearance may create opportunities. Companies such as Felix Schoeller, Koehler Paper, Drewsen Spezialpapiere, Grünewald Papier and UPM Nordland Paper all possess strong positions within specialty paper markets. They may not be able to replace every product grade produced by Coldenhove, but customers looking for reliable alternatives are likely to turn to these suppliers.

For the recovered paper sector, developments like this are equally significant. Every mill closure reduces domestic processing capacity and increases dependence on a smaller number of large consumers or export destinations. That does not create immediate disruption, but over time it makes the entire supply chain more vulnerable.

Ultimately, the bankruptcy of Coldenhove raises a broader question about the future of paper manufacturing in Western Europe. Perhaps the issue is no longer whether paper can still be produced here, but how much capacity a mill needs in order to survive. Coldenhove had a strong reputation, highly specialized products and centuries of experience. Apparently, in today’s market, that is no longer enough.

The paper industry has always been cyclical, but one trend is becoming increasingly clear: scale matters more than ever. And that may be the most important lesson to take away from the loss of one of the Netherlands’ oldest paper mills.