Monthly insights from the recovered paper and packaging markets

📉 Market Overview: A Difficult Autumn for the Paper Industry

The European recovered paper market remains subdued as we move deeper into the final quarter of the year.

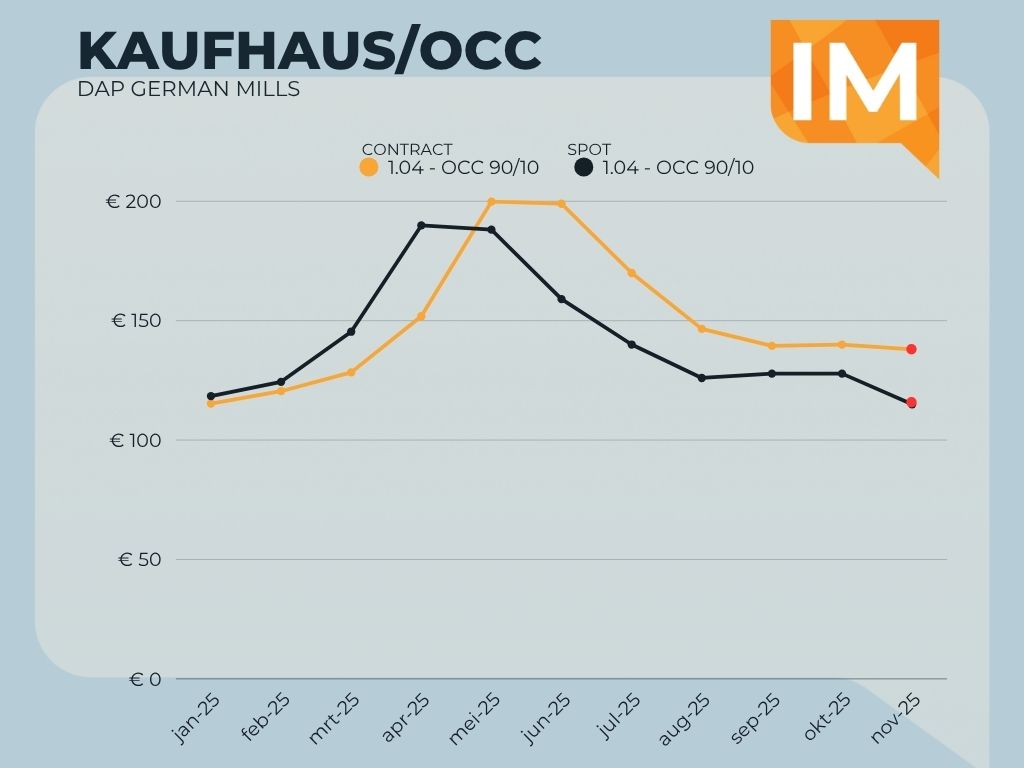

Cardboard (OCC) prices are showing a mild decline under pressure from lower export values. In Germany, price levels now range around €115–117 per ton.

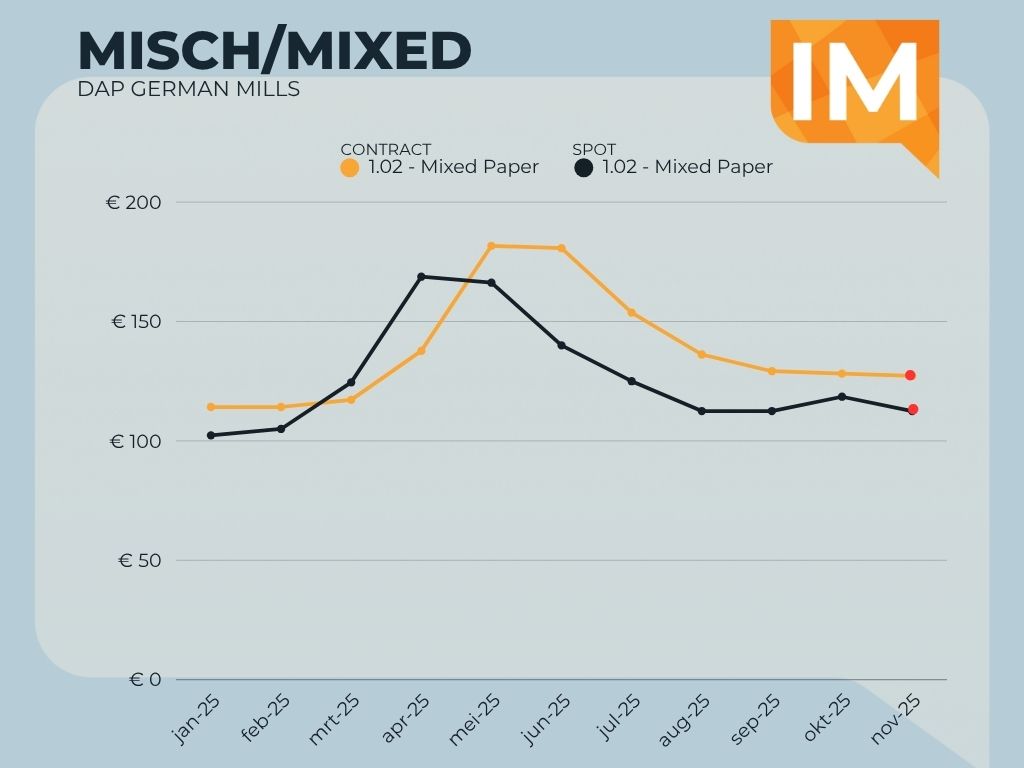

Mixed paper (1.02) remains relatively stable and well demanded, though downward corrections appear inevitable if OCC continues to weaken.

Deinking grades, once in high demand during the summer, are now struggling to find buyers. Mills have reached comfortable stock levels, and pricing pressure is intensifying.

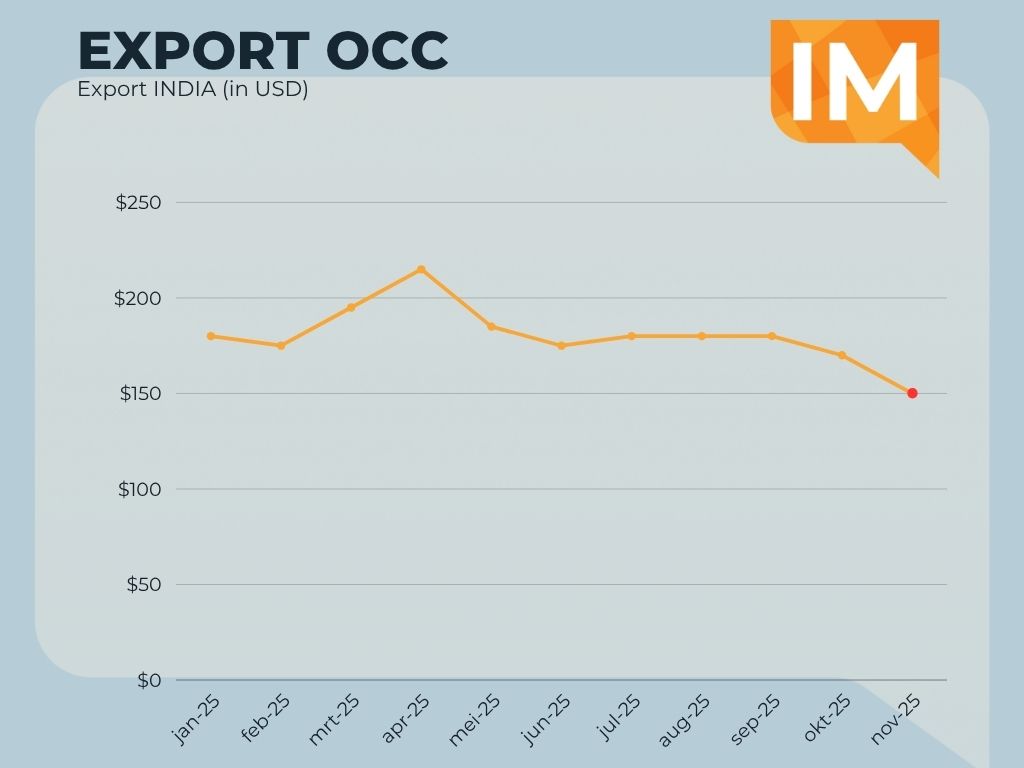

Export markets are quieter as Chinese import flows slow down. In India, prices for EOCC 95/5 have slipped to around $150 CNF per ton, with buying sentiment cautious.

The mood in the market can best be described as hesitant: little movement, low volumes, and cautious optimism that stability will return before year-end.

🗂️ “DIWASS: ist das Wass?” – Europe’s Next Bureaucratic Challenge

Last week, the Dutch IL&T (Inspection for the Environment and Transport) held its second meeting on the new EVOA regulation and the upcoming DIWASS (Digital Waste Shipment System) , the EU’s new centralized waste shipment platform.

From May 21, 2026, all waste transports (including green listed waste) must be digitally registered via DIWASS.

In theory, DIWASS is meant to simplify and harmonize European reporting. In practice, confusion dominates.

Questions persist about registration timelines, required documentation, and most crucially for traders whether a Dutch exporter can still appear as the “person who arranges the shipment” on an annex when cargo is loaded in another EU country.

Early indications suggest that DIWASS might not deliver the clarity it promises. Instead, many fear an increase in bureaucracy, multiple registrations across EU states, and potential disruptions in cross-border waste trade.

As of now, DIWASS looks less like a leap forward and more like another layer of administrative fog.

🌏 China Rejects “Recycled Pulp” Markets React

Mid-October brought unexpected turbulence to the Asian recovered paper trade.

Reports from China confirmed that 30 containers of “recycled pulp” were rejected at port inspection due to contamination and mold issues.

Since China’s ban on waste paper imports, large mills have relied on importing recycled pulp made from recovered paper in Thailand, Vietnam, and Malaysia. Two key types exist:

- Dry pulp: shredded NCC, repackaged to resemble clean fiber;

- Wet pulp: cleaned and de-inked material produced through wet pulping and filtration.

The recent rejection concerned dry pulp from Thailand, which authorities deemed “recycled waste” rather than usable fiber. The result: tighter customs controls under the relevant HS Code and widespread nervousness in regional markets.

India and Indonesia, quick to seize the narrative, used the news to negotiate lower import prices pushing EOCC 95/5 values down to $150 CNF.

Whether this becomes the new market floor or a temporary dip will depend on how China enforces its stricter import inspections in the coming weeks.

📉 A Sticky, Slow Market – and Few Bright Spots

October has been a grind for the recovered paper industry. Trading volumes remain low, price levels are sliding, and liquidity is scarce. Despite generally stable macroeconomic signals across Europe, the paper market continues to lag.

Across the supply chain from collectors to converters sentiment is subdued. Many participants describe it as “a market in slow motion.”

Why such a gap between macro data and paper reality?

Traditionally, (recovered) paper has been a reliable economic indicator: when it weakens, it signals broader slowdown. If that pattern holds true, the current softness may foreshadow further industrial strain.

Demand for office paper and Multidruck grades has weakened sharply. The latter is directly linked to the collapsing White Top Testliner segment, where demand has evaporated. The question remains: why has office paper also lost favor so abruptly?

Perhaps the public simply wants its toilet paper white again.

🔎 November Outlook

November brings little optimism to the recovered paper market.

Export prices are falling, domestic grades are under pressure, and regulatory uncertainty looms with DIWASS on the horizon. The Chinese rejection of recycled pulp adds to market nervousness, while slow trading conditions weigh on sentiment.

Still, history shows that downturns often lay the foundation for stronger rebounds.

For now, patience and a close eye on export dynamics will be key.